Chapter 22

22Written Investment Policy

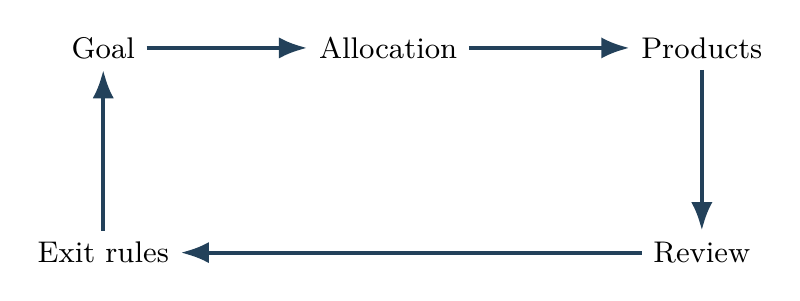

A written investment policy turns discipline into procedure. It states the goal, amount, time period, allocation, product type, review date, and exit condition. The document should be short enough to use and clear enough to follow under stress.

Goal

Example: writing "retirement at 60" is weaker than writing the monthly inflation-adjusted income needed after salary stops. A goal must describe the future cash flow or purchase clearly.

A goal is the destination in INR terms, with name, amount, date, and priority.

Without a goal, every product appears possible and every market movement feels meaningful.

Write the destination.

- Write each goal in one line.

- Separate essential goals from optional goals.

- Update goals after major life changes.

Amount

Example: a house goal must include down payment, stamp duty, registration, brokerage, interiors, and moving cost. The amount should reflect the full Indian transaction, not only the advertised price.

Amount is the required future corpus for a goal.

It must include inflation, tax, and margin for uncertainty. Underestimating amount produces false comfort.

Inflate and buffer.

- Estimate today's cost first.

- Inflate it to the goal year.

- Add buffer for important goals.

Time period

Example: an education goal due in 2034 and a vacation due next year cannot share the same risk level. Time period decides how much volatility the goal can absorb.

Time period is the number of years between now and the goal date.

Time period determines suitable risk. The same product can be wise for one goal and reckless for another.

Let time set risk.

- Record start date and target date.

- Convert vague goals into years remaining.

- Shorten risk as the deadline approaches.

Asset allocation

Example: writing 60 per cent equity and 40 per cent debt gives the portfolio a measurable risk structure. Without allocation, every market move becomes a new debate.

Asset allocation states how much goes to equity, debt, cash, gold, or other assets.

It is the central design choice. Written allocation prevents mood-based risk changes.

Write target and drift.

- Assign allocation for each goal.

- Define acceptable drift.

- Rebalance by rule.

Product type

Example: an IPS may allow broad index funds, short-duration debt funds, PPF, EPF, and bank deposits while banning leveraged trades. Product type rules prevent impulse purchases.

Product type converts allocation into Indian instruments: index funds, active funds, debt funds, bank deposits, cash, or insurance.

The product should serve the plan, not replace the plan.

Simple products first.

- Choose simple products first.

- Reject products that do not match goal, horizon, or risk.

- Record why each product exists.

Review date

Example: fixing one annual review date stops constant tinkering while still allowing course correction. The date turns discipline into a calendar event.

Review date is the scheduled measurement point for the plan.

It prevents both neglect and obsessive checking. A good system has periodic calibration, not continuous anxiety.

Schedule review.

- Set annual review dates.

- Review after major income, family, or health changes.

- Do not review long-term plans daily.

Exit condition

Example: an exit condition can say sell when the goal is fully funded, when allocation breaches a band, or when the product violates its mandate. Exit rules make selling a process instead of a reaction.

Exit condition defines when to sell, switch, stop, or reduce risk.

Exit rules turn discipline from intention into procedure.

Write exit triggers

- Write exit rules for goal completion, drift, product failure, and life change.

- Include tax and liquidity constraints.

- Follow the written rule unless facts truly change.