Chapter 1

1Personal Finance Foundation

This chapter builds the investment system from the cash-flow base. The order is deliberate: first identify income and expenses, then measure savings rate, then impose a budget, then protect the system with an emergency fund. Only after that does debt quality and lifestyle inflation become meaningful, because both decide whether future cash flow remains free for investing.

Income and expenses

Example: a salaried Indian household may see salary credit, rent, school fees, UPI spending, EMIs, and insurance premiums passing through the same bank account. Separating these flows shows the first invariant of investing: only the monthly surplus can become capital.

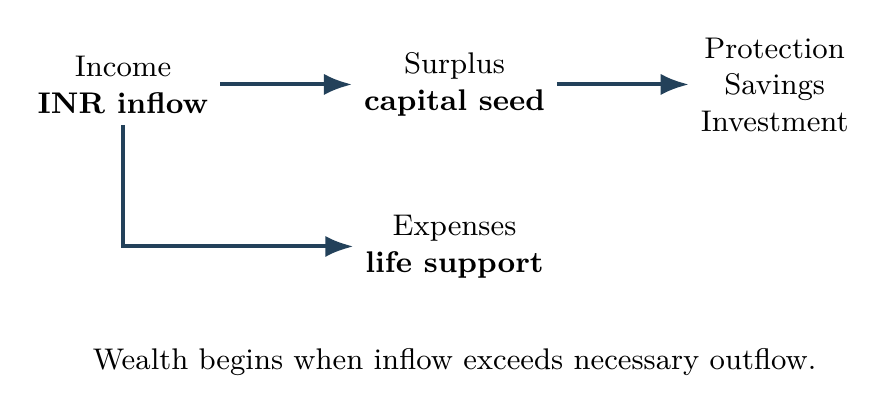

Income is INR inflow: salary, professional fees, rent, pension, business income, or interest. Expenses are INR outflows required for life, obligations, and choices.

Investment capital is not created by return first; it is created by surplus first. In physics language, income is input current, expenses are load, and surplus is the energy left for storage and future work.

Surplus measurement.

- Measure monthly inflow and outflow before choosing any Indian investment product.

- Classify expenses as fixed, variable, discretionary, and avoidable.

- Surplus = income minus expenses; it is a measured value, not a feeling.

Savings rate

Example: if monthly take-home income is INR 1,00,000 and INR 25,000 is moved to an index fund SIP, PPF, or emergency fund before spending begins, the savings rate is 25 per cent. That number matters more than a clever product in the first few years.

Savings rate is the fraction of take-home income retained for future use:

\[ \text{savings rate}=\frac{\text{monthly savings}}{\text{monthly take-home income}}. \]Return acts on capital, but savings creates capital. In the early phase, raising savings rate usually has more effect than searching for a slightly higher return.

Pay future self first.

- Move savings out of the spending account soon after income arrives.

- Increase savings rate gradually so the system remains stable.

- Count money as saved only after it is separated from casual spending.

Budgeting

Example: many Indian families budget around rent, groceries, parents' support, tuition, travel, and festivals. A usable budget reserves money for these real outflows first, then prevents casual app payments and lifestyle upgrades from absorbing the investable surplus.

A budget is a pre-decided allocation of income across essentials, protection, goals, repayments, and free spending.

A useful budget is not moral policing. It is a boundary condition that prevents emotion, fatigue, and social pressure from assigning money randomly.

Simple budget rule.

- Build the budget from actual past spending, not ideal spending.

- Automate essentials, insurance premiums, debt repayments, and investments.

- Keep a small free-spending region; rigid systems break quickly.

Emergency fund

Example: during a job gap or hospital admission, a person should not be forced to redeem equity mutual funds during a market fall. A bank deposit or liquid fund buffer keeps the investment plan separate from the emergency.

An emergency fund is low-risk, liquid INR money reserved for shocks such as job loss, medical gaps, urgent travel, or repairs.

Shock absorber

The emergency fund is a buffer capacitor. It absorbs sudden cash demand so long-term investments are not sold at the wrong time.

Liquidity before return

- Keep 6 to 12 months of essential expenses if income is uncertain.

- Use RBI-regulated bank savings, sweep deposits, fixed deposits, or high-quality liquid funds.

- Refill the fund before increasing investment risk.

Good debt vs bad debt

Example: a home loan on an affordable flat may create durable utility, while a personal loan for a depreciating phone or vacation converts future salary into past consumption. The EMI tells whether the debt strengthens life or weakens future surplus.

Debt shifts future income into the present. Good debt funds durable utility or productive capacity. Bad debt funds fast depreciation, status, or avoidable consumption.

Every EMI is a claim on future surplus. Debt is acceptable only when the financed object is useful and the repayment does not damage protection, savings, or goal investing.

Debt test.

- Good debt has purpose, affordability, and a clear end date.

- Bad debt reduces future freedom without creating durable value.

- EMI should not compress emergency funding, insurance, or SIP discipline.

Lifestyle inflation

Example: when salary rises from INR 12 lakh to INR 18 lakh, wealth does not rise automatically if rent, car EMI, eating out, and gadgets rise with it. Capturing part of each increment into SIPs turns income growth into capital growth.

Lifestyle inflation is the automatic rise of expenses when income rises. The person earns more, but the investable surplus does not grow.

Income growth creates wealth only when expenses grow slower than income. The gap between the two is the engine that powers long-term investing.

Raise allocation.

- Pre-commit part of every raise to savings and investing.

- Upgrade life selectively, not reflexively.

- Protect savings rate from comparison-driven spending.