Chapter 2

2Protection Before Investment

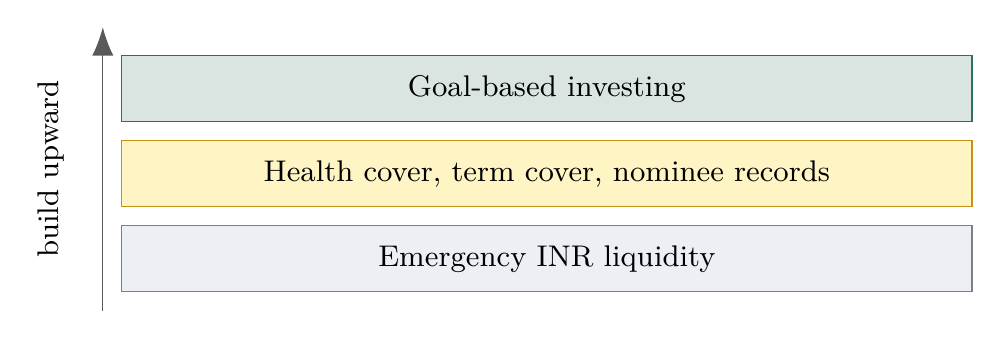

Investment should begin only after the household is protected from shocks that can destroy capital. This chapter moves from health risk to income-loss risk, then to nomination and medical liquidity, and finally separates insurance from investment. The logic is simple: first prevent ruin, then pursue return.

Health insurance

Example: one private hospital bill in India can consume years of savings if insurance is absent or too small. Health cover protects the investment base by transferring large medical uncertainty away from the portfolio.

Health insurance is an IRDAI-regulated contract that pays eligible medical costs according to its policy wording, exclusions, waiting periods, and claim process.

For an Indian resident, hospital expenses can rise faster than general inflation. One large admission can consume years of savings if the household depends only on cash reserves.

Risk pooling

Insurance transfers a large uncertain cost from one household to a pool. The premium is a known small loss paid to avoid a rare but financially destructive loss.

Health cover before market risk

- Buy adequate health cover before taking meaningful equity risk.

- Check exclusions, waiting periods, network hospitals, room-rent limits, and claim service.

- Treat employer cover as useful but incomplete because employment can change.

Term insurance

Example: a resident with dependents and a home loan needs income replacement more than a bundled savings policy. A plain term plan keeps the family goal funded even if the earning member dies early.

Term insurance is pure life cover. It pays a sum assured to the nominee if the insured person dies during the policy term and the claim is valid.

Term insurance is needed only when someone depends on your income. The cover is not for you; it replaces the economic support your family would lose.

Human capital replacement

The correct cover is linked to the present value of future household support: expenses, liabilities, education needs, and time left until dependents become independent.

Keep life cover pure.

- Buy term insurance only if dependents rely on your income.

- Prefer large cover, low premium, and simple terms over investment-linked complexity.

- Reassess cover when liabilities, dependents, or accumulated assets change.

Nominee

Example: after a sudden death, a nominee in bank accounts, mutual funds, EPF, and demat records helps the family claim assets without searching through papers. Nomination is not wealth creation, but it prevents wealth from becoming inaccessible.

A nominee is the person recorded to receive account proceeds or assist transfer after death, subject to Indian legal rules.

Nomination is operational hygiene. It does not replace a will or succession law, but it prevents avoidable friction when family members are already under stress.

Nomination hygiene.

- Add nominees to Indian bank, demat, mutual fund, and insurance accounts.

- Update nomination after marriage, birth, death, separation, or other major life changes.

- Tell trusted family members where financial records are stored.

Emergency medical fund

Example: insurance may involve exclusions, waiting periods, co-payments, or delayed reimbursement. A dedicated medical cash buffer pays the first bills while the claim process catches up.

An emergency medical fund is quick-access money kept for deductibles, co-pay, non-covered items, tests, medicines, travel, and claim-settlement delays.

This fund is separate from the main emergency fund because medical timing is not negotiable. Even with insurance, hospitals may require immediate cash flow.

Medical liquidity.

- Keep medical gap money in a bank account or similarly liquid low-risk place.

- Do not invest this money in equity or volatile debt.

- Rebuild it after use.

Why insurance is not investment

Example: many traditional policies mix small life cover with low-return savings and opaque charges. For most Indian households, buying protection separately and investing separately keeps both decisions measurable.

Insurance and investment solve different problems. Insurance prevents ruin from low-frequency high-impact events. Investment grows surplus capital for goals.

Different equations

Combining insurance and investment often produces weak protection and opaque returns. A cleaner system uses term cover for risk transfer and transparent Indian investment products for growth.

Do not mix purpose.

- Buy insurance for protection, not maturity value.

- Compare investments by return, cost, liquidity, tax, and risk.

- Avoid products whose cash flows cannot be explained simply.