Chapter 4

4Risk and Return

Risk is not one object. It has different sources: market movement, inflation, liquidity, credit, interest rates, and investor behavior. This chapter separates those forces so return can be understood as compensation for bearing the right kind of risk for the right amount of time.

Market risk

Example: Indian equity investors saw sharp falls in 2008 and again in March 2020, even in good companies and diversified funds. The practical question is not whether prices fall, but whether the money has enough time to wait for recovery.

Market risk is the fluctuation of Indian asset prices due to changing expectations, liquidity, earnings outlook, interest rates, and crowd behavior.

Price and value

Price is a measurement made by buyers and sellers today. Value is linked to future cash-flow capacity. Their mismatch creates volatility.

Accept volatility only with time

- Accept market risk only for money with enough time.

- Diversify instead of predicting every price move.

- Treat volatility as expected behavior, not system failure.

2008 - Global financial crisis

Equity markets across the world fell sharply as the US housing and credit system broke. The event showed that market risk is not theoretical: prices can fall quickly even when investors believed risk was dispersed.

Inflation risk

Example: a savings account balance may stay numerically stable while rent, food, electricity, and healthcare costs rise. For an Indian resident, money that earns below inflation after tax is losing real purchasing power.

Inflation risk is the loss of INR purchasing power. Money can be numerically safe and economically unsafe at the same time.

If return is below inflation after tax, real value decays even when the account balance looks stable.

Judge real value.

- Judge return after inflation and tax.

- Hold growth assets for long-term purchasing power.

- Do not confuse stable balance with stable value.

Liquidity risk

Example: a flat, land parcel, or locked-in product may show high value on paper but fail to produce cash when a fee or medical bill is due. Liquidity is the ability to get money at the needed date without distress pricing.

Liquidity risk is the inability to convert an asset into cash quickly at a fair price.

Liquidity risk appears when timing is forced. An asset can be valuable in theory and still unusable if buyers are absent when cash is needed.

Match liquidity to need.

- Match liquidity with the goal date.

- Keep emergency money in highly liquid form.

- Demand higher expected return for illiquid assets.

Credit risk

Example: an extra yield in a debt fund or company deposit can hide borrower weakness. Indian investors learned through several defaults that fixed-income products can carry real default risk.

Credit risk is the chance that a borrower fails to pay interest or principal. It applies to bonds, deposits outside protected limits, and debt funds.

Yield is not free

Higher yield often means lower credit quality, longer maturity, weaker liquidity, or structural complexity. Extra yield is compensation for risk, not free energy.

Do not chase yield blindly

- Check credit quality before chasing return.

- Prefer safety over small extra return for short-term debt.

- Diversify credit exposure.

2018 - IL&FS default in India

The default exposed credit and liquidity stress in parts of the Indian debt market. It reminded investors that debt funds are not identical to bank deposits.

Interest-rate risk

Example: when RBI policy rates rise, long-duration bond funds can show negative returns even without any default. The bond is paying, but its market price changes because newer bonds offer higher yields.

Interest-rate risk is the fall in bond price when market interest rates rise. Longer-duration bonds usually move more.

Duration is like sensitivity. If cash flows are locked farther into the future, the present price reacts more strongly to rate changes.

Respect duration.

- Use short-duration debt for near goals.

- Understand duration before buying debt funds.

- Do not assume all debt products are stable.

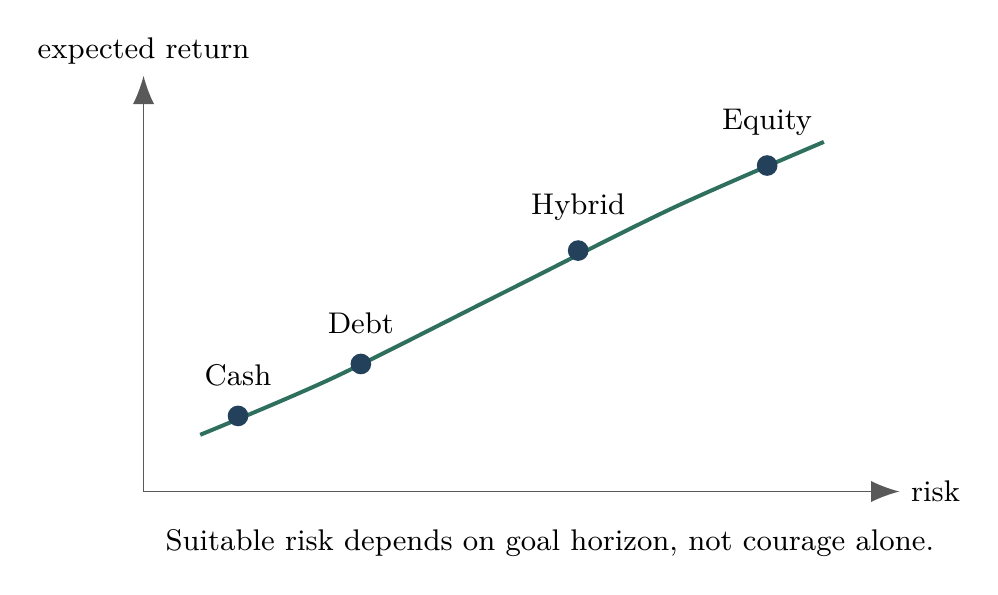

Risk tolerance

Example: an investor who says equity is acceptable in a rising market may panic when a INR 10 lakh portfolio becomes INR 7 lakh. Real risk tolerance is revealed by behavior during drawdowns, not by forms filled in calm periods.

Risk tolerance is the amount of volatility and loss an investor can financially and psychologically survive.

Capacity depends on time horizon, income stability, dependents, and emergency money. Temperament is revealed during falling markets, not rising markets.

Holdable risk only.

- Choose allocation you can hold during a drawdown.

- Lower risk if panic would force selling.

- Increase risk only after understanding the possible loss range.