Chapter 5

5Time Horizon

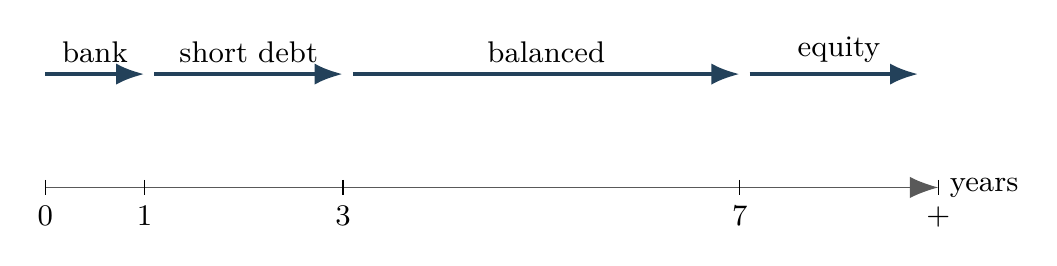

Time horizon is the bridge between goals and products. Money needed soon requires safety and liquidity. Money needed much later can accept volatility for growth. This chapter orders horizons from less than one year to more than seven years, then gives the matching rule.

Less than 1 year

Example: money needed for tax, rent deposit, school fees, or a planned trip within a year belongs in savings, fixed deposits, or liquid instruments. Equity risk has too little time to repair a bad entry point.

This is money required almost immediately, with no meaningful recovery time.

The investment problem is capital preservation and liquidity. Return is secondary because even a small loss can disturb the goal.

No volatility bucket.

- Use Indian savings accounts, fixed deposits, or liquid funds.

- Avoid equity and long-duration debt.

- Keep the money simple and visible.

1--3 years

Example: for a car or professional course planned in two years, capital protection dominates return. Short-duration debt and bank deposits fit better than volatile equity funds.

This horizon permits modest yield improvement but still cannot tolerate large price movement.

The useful question is: can this product be down exactly when the cash is needed? If yes, the product does not belong in this bucket.

Stability first.

- Prefer Indian bank deposits or high-quality short-duration debt funds.

- Keep equity exposure near zero unless the goal is flexible.

- Check exit load and taxation before investing.

3--7 years

Example: a five-year home down-payment goal may allow limited equity exposure, but not an aggressive equity-only plan. The allocation should reduce risk as the purchase date approaches.

This is a transition zone where some growth may be useful but deadline risk is real.

Some equity may help beat inflation. As the date approaches, uncertainty must be converted into certainty.

De-risk gradually.

- Use balanced allocation according to goal flexibility.

- Reduce risk gradually in the final years.

- Do not wait until the last month to de-risk.

7+ years

Example: retirement twenty years away can use equity because business growth has time to work through cycles. The same equity fund may be unsuitable for money needed next Diwali.

This is a long horizon where productive ownership assets have time to work through cycles.

Time and business growth

Equity suits this region because companies can grow earnings over many business cycles. Volatility remains, but time improves the chance that growth dominates noise.

Growth bucket.

- Use diversified equity as the main growth engine.

- Keep investing during corrections.

- Review allocation, not daily price.

Matching product with time period

Example: using ELSS for three-year tax lock-in, PPF for long disciplined savings, and liquid funds for emergencies shows product matching. The product is judged by the goal's time period, not by popularity.

Every product has a natural time scale. Mismatch creates avoidable risk: equity for short goals, cash for retirement, or illiquid assets for urgent money.

Time-scale matching

Discipline is matching the time constant of the product to the time constant of the goal.

Horizon before product

- First define the horizon, then select the product.

- Short horizon needs liquidity and safety.

- Long horizon needs inflation-beating growth.