Chapter 10

10Diversification

Diversification reduces dependence on one uncertain outcome. This chapter moves from broad asset diversification to sector, company, and fund-house diversification, then ends with concentration risk.

Across assets

Example: holding only equity exposes a family to market drawdowns; holding only deposits exposes it to inflation. Mixing equity, debt, cash, and sometimes gold spreads risk across different engines.

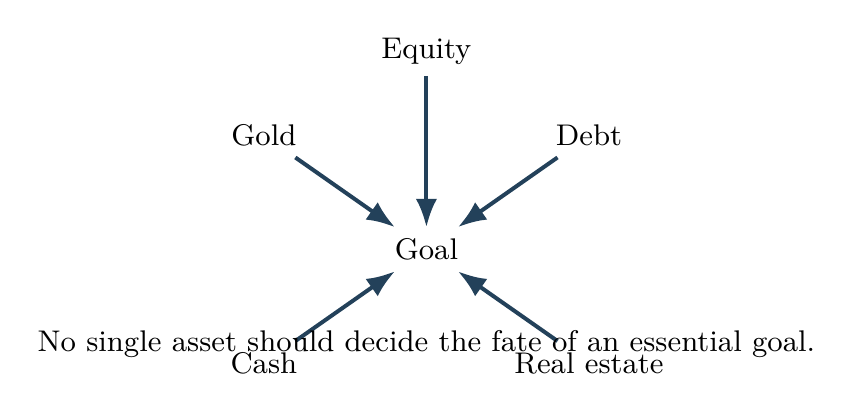

Asset diversification means holding assets whose risk sources are not identical.

Different forces

Equity, debt, gold, real estate, and cash respond to different forces. Diversification reduces dependence on one outcome without requiring perfect prediction.

Use roles, not clutter.

- Hold assets with different roles.

- Do not diversify so much that the plan becomes unmanageable.

- Remember diversification reduces risk; it does not remove loss.

Across sectors

Example: a portfolio concentrated only in banks or IT can suffer when that sector faces regulation, margin pressure, or valuation decline. Sector diversification reduces dependence on one economic story.

Sector diversification avoids dependence on one part of the Indian economy.

Banking, IT, energy, pharma, consumption, and manufacturing can move differently. Sector concentration is a hidden bet on one cycle.

Avoid theme dependence.

- Prefer broad funds unless you understand sector risk.

- Avoid putting most equity money into one theme.

- Check sector weights in funds.

Across companies

Example: a single-stock portfolio can be damaged by fraud, disruption, debt stress, or management failure. Mutual funds and index funds reduce this company-specific risk.

Company diversification reduces damage from one company's failure, fraud, debt stress, disruption, or management error.

The market rewards ownership of productive businesses, not blind faith in one name.

Limit single-name risk.

- Avoid excessive exposure to one stock.

- Use diversified mutual funds or index funds for simplicity.

- Treat employer stock as concentration if salary also comes from that company.

Across fund houses

Example: even regulated Indian fund houses can differ in process, risk controls, and operational decisions. Spreading large holdings across sound AMCs reduces dependence on one institution.

Fund-house diversification reduces operational and style dependence across asset managers.

It matters more when using active funds. But owning many similar funds from many houses may only duplicate holdings.

Diversify without clutter.

- Use a few reliable fund houses, not dozens.

- Check overlap before adding a new fund.

- Diversify operations without cluttering the portfolio.

Avoiding concentration

Example: employees often accumulate company stock, ESOPs, salary dependence, and career risk in the same employer. Diversification outside that employer prevents one failure from damaging both income and wealth.

Concentration means one stock, sector, property, fund style, or asset class can dominate the portfolio outcome.

Concentration increases both possible gain and possible ruin. It is powerful only when backed by deep knowledge and ability to absorb loss.

Essential goals need dispersion

- Limit exposure to any single stock, sector, or property.

- Reduce concentrated positions gradually and tax-aware.

- Never concentrate money required for essential goals.