Chapter 9

9Asset Allocation

Asset allocation decides the growth-stability structure of the portfolio. The chapter begins with the equity-debt ratio, then compares age-based and goal-based allocation, and finally describes conservative, moderate, and aggressive portfolios.

Equity-debt ratio

Example: a 70:30 equity-debt portfolio behaves differently from a 30:70 portfolio during a crash. The ratio is the main control knob for volatility and long-term growth.

The equity-debt ratio is the percentage split between growth assets and stabilizing assets.

Dominant design variable

Portfolio behavior is dominated more by allocation than by product selection. Indian equity supplies long-term growth; Indian debt supplies ballast.

Choose ratio from goal and temperament.

- Choose the ratio from goal horizon and risk tolerance.

- Increase debt as a fixed goal approaches.

- Rebalance when the ratio drifts materially.

Age-based allocation

Example: a 28-year-old with stable income and no near goal may hold more equity than a 60-year-old beginning withdrawals. Age is a useful proxy because human capital and recovery time change.

Age-based allocation is a shortcut that reduces equity as age rises.

It is useful as a starting estimate because younger investors usually have more income years ahead. It is incomplete because income security, dependents, goals, and temperament also matter.

Use age as input, not command.

- Use age only as a starting estimate.

- Adjust for job stability and liabilities.

- Do not hold high equity merely because a formula says so.

Goal-based allocation

Example: the same person can hold equity for retirement, debt for a three-year house goal, and cash for emergencies. Allocation should follow the date and importance of each goal.

Goal-based allocation assigns each goal its own risk profile and product set.

Retirement, house down payment, education fees, and emergency money should not share one blind allocation.

Separate by goal

- Create separate buckets by goal and date.

- Match each bucket to its horizon.

- Review buckets independently.

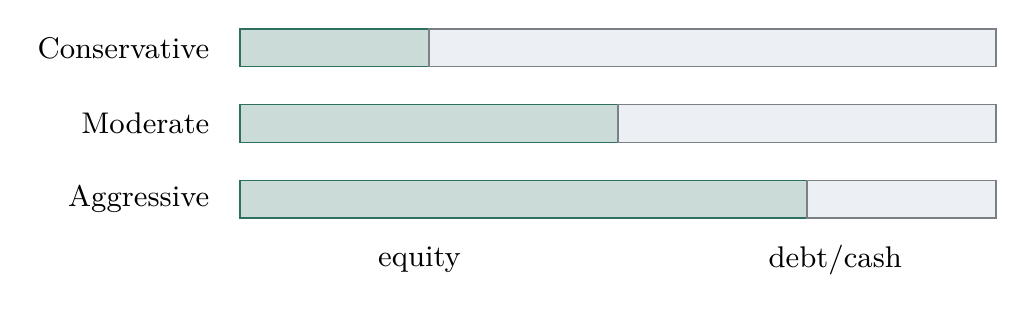

Conservative portfolio

Example: an investor supporting parents, paying EMI, and saving for a near goal may choose a debt-heavy portfolio. Lower return is acceptable if it prevents forced selling.

A conservative portfolio prioritizes capital stability and lower drawdown.

It suits near goals, low risk tolerance, or uncertain income. It accepts lower expected return to reduce emotional and financial stress.

Stability dominant.

- Keep debt and cash dominant.

- Use limited equity only for inflation protection if horizon allows.

- Avoid products that can surprise on the downside.

Moderate portfolio

Example: a middle-career salaried investor with emergency money and goals beyond five years may mix equity and debt. The portfolio seeks growth but keeps enough stability to stay invested.

A moderate portfolio balances growth and stability.

It accepts meaningful volatility but avoids extreme dependence on equity. It suits investors with medium or long horizons and stable behavior.

Balanced discipline.

- Combine diversified equity with quality debt.

- Rebalance at defined intervals.

- Do not keep changing allocation with headlines.

Aggressive portfolio

Example: an investor with high income stability, long horizon, and no near withdrawal need may accept high equity exposure. Aggression is justified only when drawdowns can be held without panic.

An aggressive portfolio seeks higher long-term growth through high equity exposure.

It can fall deeply in bad markets. It works only if the investor has long horizon, stable income, and the ability to hold through fear.

Aggression needs capacity.

- Use aggressive allocation only for long-term goals.

- Prepare mentally for large drawdowns.

- Keep emergency and near-goal money outside it.