Chapter 8

8Asset Classes

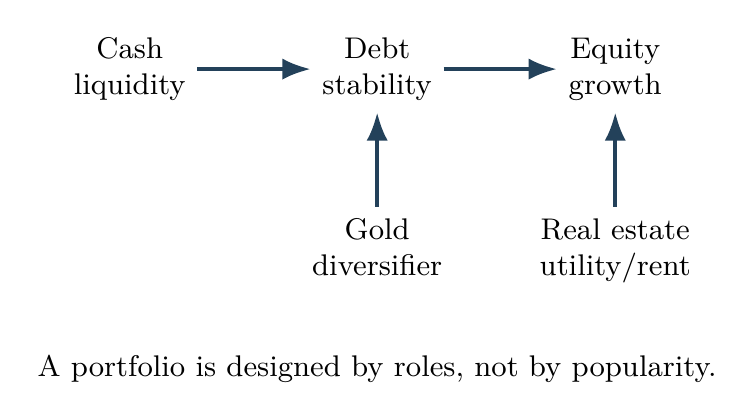

Asset classes are the basic materials of a portfolio. Each one has a job: equity for growth, debt for stability, gold for diversification, real estate for utility or rent, cash for liquidity, fixed deposits for known return, and bonds for structured lending.

Equity

Example: buying an equity mutual fund means owning slices of businesses such as banks, IT companies, manufacturers, and consumer firms. The return source is business growth, but the price path is volatile.

Equity is ownership in businesses listed or accessible through Indian markets such as NSE and BSE.

Return comes from earnings growth, dividends, and change in valuation. Equity is volatile because business expectations change, but over long periods it can participate in economic growth.

Use equity for growth

- Use equity for long-term goals.

- Diversify because individual businesses can fail.

- Expect drawdowns as part of ownership.

Debt

Example: a government bond, corporate bond, or debt fund lends money and expects interest plus principal. It is usually steadier than equity, but credit, duration, and liquidity still matter.

Debt is lending to the Government of India, state entities, banks, companies, or money-market borrowers.

Return comes from interest and repayment of principal. Debt is usually less volatile than equity, but it has credit, rate, liquidity, and reinvestment risks.

Use debt for stability

- Use debt for stability and near-term goals.

- Check credit quality and duration.

- Do not chase yield blindly.

Gold

Example: Indian families often hold gold for tradition and crisis comfort; modern investors may use sovereign gold bonds or gold ETFs. Gold does not produce cash flow, but it can diversify currency and crisis risk.

Gold is a non-productive asset widely held in India. It does not generate cash flow.

Its value comes from scarcity, trust, currency perception, and crisis demand. It may diversify a portfolio because it can behave differently from equity and debt.

Small diversifier.

- Use gold as a small diversifier, not the main engine.

- Prefer efficient investment forms over jewellery when the purpose is investment.

- Do not expect regular income from gold.

Real estate

Example: a flat can provide use, rent, or appreciation, but it comes with registration cost, maintenance, tax, low liquidity, and large ticket size. Real estate is both an asset and a location-specific commitment.

Real estate is a physical Indian asset that can provide utility, rent, or appreciation.

It is lumpy, illiquid, paperwork-heavy, and location-dependent. High transaction cost and leverage make errors expensive.

Avoid property concentration.

- Separate house-for-use from investment property.

- Include maintenance, tax, vacancy, and loan cost.

- Avoid overconcentration in one property.

Cash

Example: cash in a bank account lets a family pay rent, groceries, fees, and emergencies without selling investments. Its value is flexibility, not long-term growth.

Cash and bank balance give maximum liquidity and minimum market volatility.

Cash is an option: it lets you act when time matters. Its weakness is inflation, so it is not designed for long-term growth.

Use cash as a tool.

- Hold cash for emergencies and planned spending.

- Avoid excessive idle cash for long-term goals.

- Treat cash as a tool, not a strategy.

Fixed deposits

Example: Indian bank fixed deposits provide known maturity value and are familiar to households. They suit stability needs, but post-tax return may fail to beat inflation for long goals.

Indian fixed deposits offer known interest over a fixed period.

They are simple and useful for safety-oriented goals. Their real return may be modest after tax, so they suit stability more than wealth creation.

Match maturity.

- Match FD maturity with cash need.

- Check premature withdrawal rules.

- Consider tax before comparing returns.

Bonds

Example: RBI Retail Direct allows individuals to access government securities, while debt funds bundle many bonds. Bonds create predictable cash-flow claims, but their prices still move with rates and credit perception.

Bonds are tradable Indian debt instruments with coupon, maturity, yield, duration, credit quality, and market price.

Their price changes with interest rates, credit perception, and liquidity. Holding to maturity reduces price concern only if the issuer pays as promised.

Understand bond risk.

- Understand coupon, maturity, yield, duration, and credit rating.

- Use high-quality bonds for conservative needs.

- Avoid complexity unless the risk is understood.